Private Equity Is Consolidating Home Services. The Best Owners Aren't Rushing to Sell.

Eric Engebretsen

•

June 15, 2026

Private equity has developed a serious appetite for home services. In Hire Bloom's 2026 Home Services Survey, 53% of operators said a private equity firm or consolidator had approached them in the past year — and 28% had been approached three or more times. Across HVAC, roofing, plumbing, pest control, and the rest of the trades, the buyout pitch has gone from rare to routine.

Now, it's a quarterly inbound.

But the most revealing finding isn't how often owners get the call. It's what the best-run operators do with it. They don't rush to sell. They build the kind of operation that earns a premium multiple — or the freedom to say no. This is a look at the money pouring into home services, and the quieter strategy underneath it.

Consolidation stopped being a someday story — it's a quarterly inbound

For many home services companies, "getting bought" was a someday conversation. Not anymore.

More than half of the operators in our survey had fielded an approach from a private equity firm or consolidator in the last 12 months; more than a quarter had fielded three or more. When the call comes every quarter, it stops being an event and becomes a backdrop.

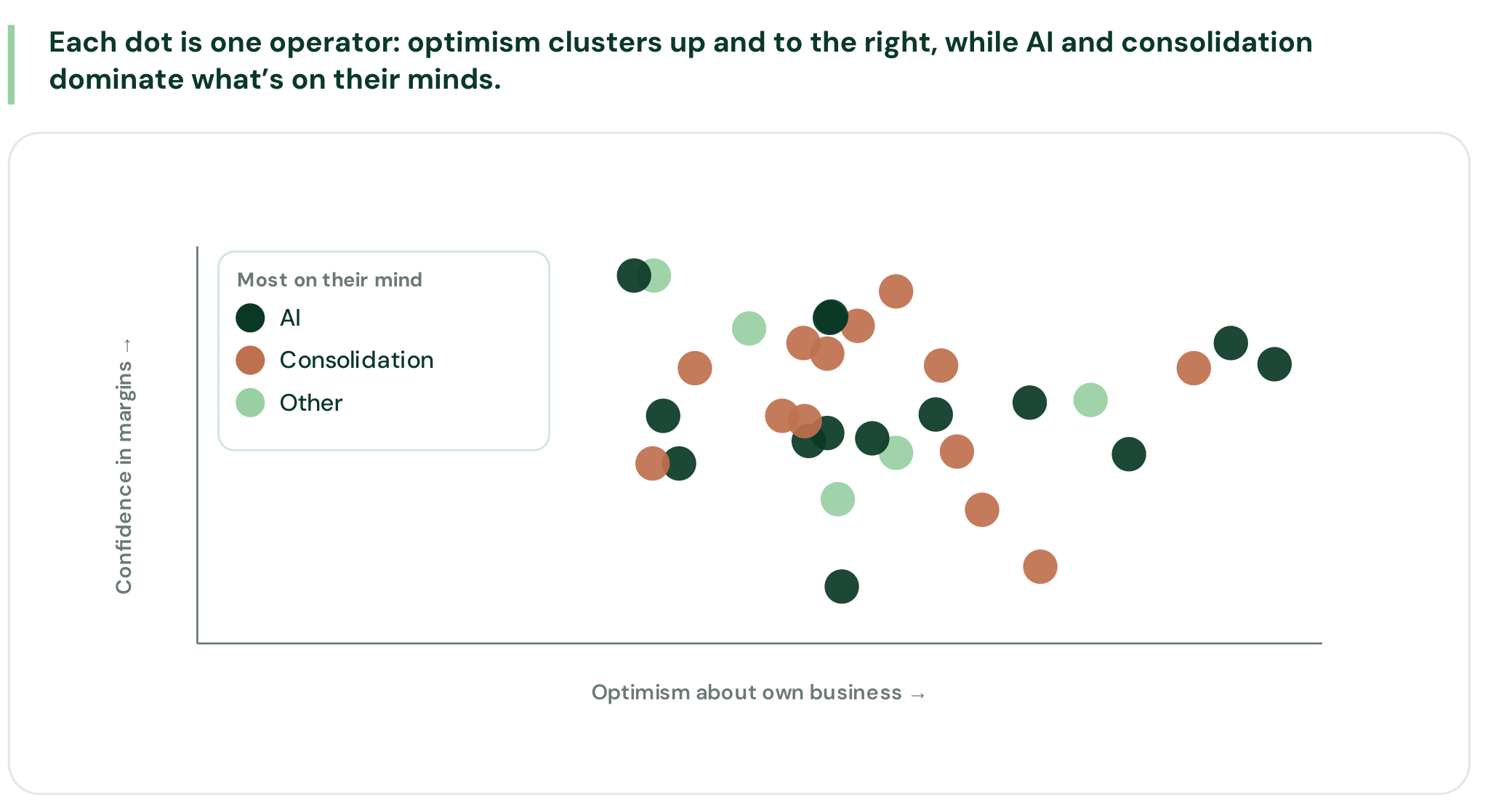

And the pressure isn't only financial. Asked what was most on their minds heading into 2026, operators named AI first at 44%, with industry consolidation right behind at 41%. Owners are bullish on their own businesses and uneasy about the forces reshaping the industry around them. Bullish and nervous, all at once.

The money behind the calls: 27 roll-ups and a $2.5B deal

The capital is substantial — and HVAC is leading the charge. There are 27 active HVAC-led roll-up platforms competing for deals right now, and in February 2026 Blackstone acquired Champions Group for roughly $2.5 billion — an implied 18.5× EBITDA (CT Acquisitions, Private Equity in HVAC 2026). HVAC is the most visible front, but the same consolidation wave is moving through roofing, plumbing, and the rest of the trades.

That kind of multiple is striking for a home services business — and it isn't evenly available. Valuations climb sharply with scale. The biggest platforms command the richest multiples, which is part of why the largest operators can afford to be patient about everything else.

For a $5M or $20M shop, that's both sobering and clarifying: the headline numbers in the press releases belong to companies several times their size. The path to a number like that runs through growth and operational discipline — not the first offer in the inbox.

The tell: after enough calls, owners worry about AI more than the sale

Here's the finding that reframes the whole conversation.

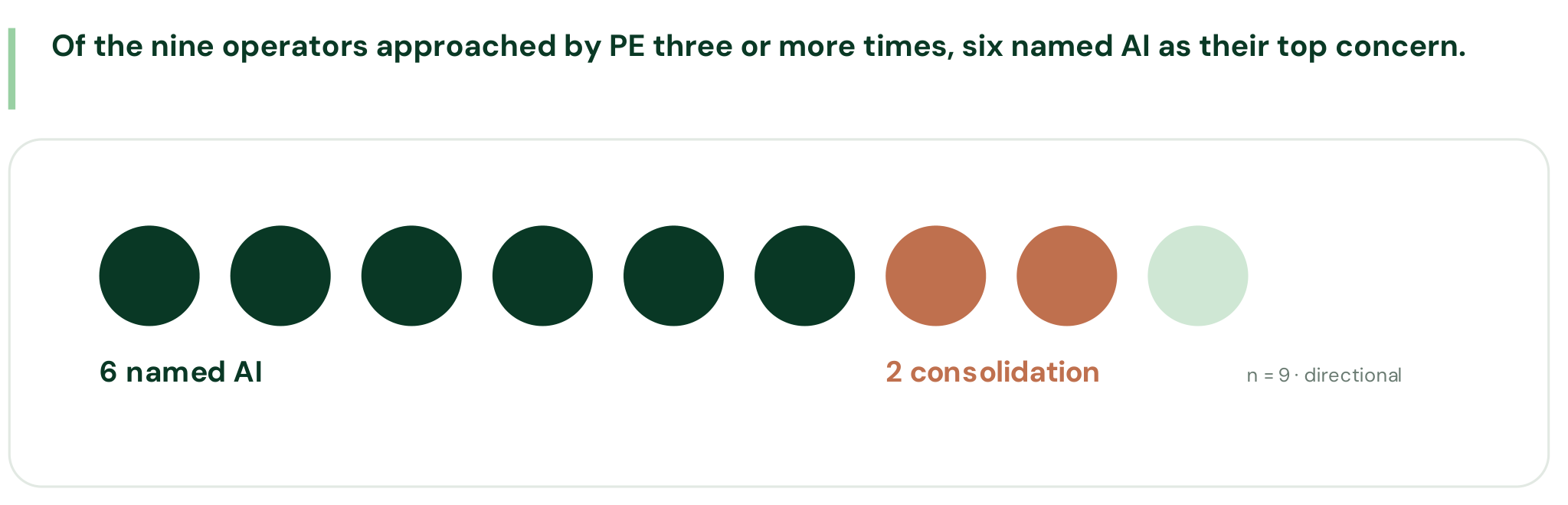

Among operators approached three or more times, AI has overtaken consolidation as the thing most on their minds. Of the nine operators in our survey who'd been approached that often, six named AI as their top concern — only two named consolidation. The group is small, so read it as a signal rather than a statistic. But it's an intuitive one.

Once you've heard the consolidation story enough times, the question stops being whether you'll be bought. It becomes what your operation needs to look like — with or without an exit. And increasingly, that's a question about how deliberately you run the business.

What acquirers are really buying: margins and retention

Strip away the deal noise and what buyers pay up for is boring: durable margins and a business that doesn't fall apart when the founder steps back. That's where the survey's most counterintuitive result matters.

The operators using AI most broadly are the smallest ones — about 3.6 to 3.8 use cases each. The largest operators average roughly 2.1, and they posted the strongest margin gains of any revenue band. The biggest operators aren't winning by adopting AI fastest. They're winning by adopting it most deliberately — and by fixing the unglamorous parts of the operation that actually move margin: dispatch, scheduling, billing, and the front office.

Retention is the other lever. Margins live or die on whether a company keeps its people, and turnover in entry-level operations roles runs as high as 70%. An operation that burns through its back office every year is worth less — to a buyer, and to the owner who keeps it.

How Best Choice Roofing scaled operations

At Hire Bloom, we help home services operators close this gap. We embed dedicated, US-educated CSRs, dispatchers, and billing specialists — sourced from BYU-Pathway — directly into the business, at a flat $13/hour with 86% first-year retention. That combination does two things a buyer notices: it protects margin, and it builds an operation that runs on systems rather than heroics.

Best Choice Roofing is a clear example of the build-don't-just-sell mindset. CEO Bryce Barnett ran the AI playbook on his estimating team, got partway, then added 15+ embedded team members on top of a tighter software stack. Throughput on insurance contingencies went from under 25% to over 80% — more than 3x — with people doing the parts AI couldn't. His rule for every tooling decision: "It doesn't have to be 'or.' It's always 'and.'" That's what a more valuable operation looks like, whether or not it's ever for sale. (Read the full Best Choice Roofing story)

Want the full picture? The patterns here — PE pressure, the AI mismatch, and the margin gap between operators — come from Hire Bloom's State of Home Services 2026, a field reading of where the market is actually heading. Download the free report.

Frequently Asked Questions

Why is private equity buying up home services companies?

add

Home services offers recurring revenue, fragmented ownership, and essential, recession-resistant demand — ideal conditions for roll-ups. PE has been most aggressive in HVAC, where there are 27 active roll-up platforms and deals like Blackstone's ~$2.5B Champions Group acquisition (18.5× EBITDA). In Hire Bloom's 2026 survey, 53% of operators across the trades had been approached in the past year.

Should I sell my home services business to private equity?

add

That's a personal and financial decision — Hire Bloom isn't a financial advisor. What the data suggests is that the strongest negotiating position comes from a disciplined operation: improving margins, low turnover, and systems that run without the founder. Those same fundamentals give you the leverage to command a higher multiple or to comfortably say no.

What multiple do home services companies sell for in a private equity deal?

add

It varies widely with size and profitability. Headline platform deals have reached 18.5× EBITDA, but those multiples are reserved for large, well-run operators; smaller shops typically transact for far less. Valuations climb sharply with scale, which is why operational discipline and growth matter more than timing the market.

.png)

.avif)